How hybrids and EVs create new revenue streams in the aftermarket, Auto News, ET Auto

By Anuj Monga and Pranav Nair

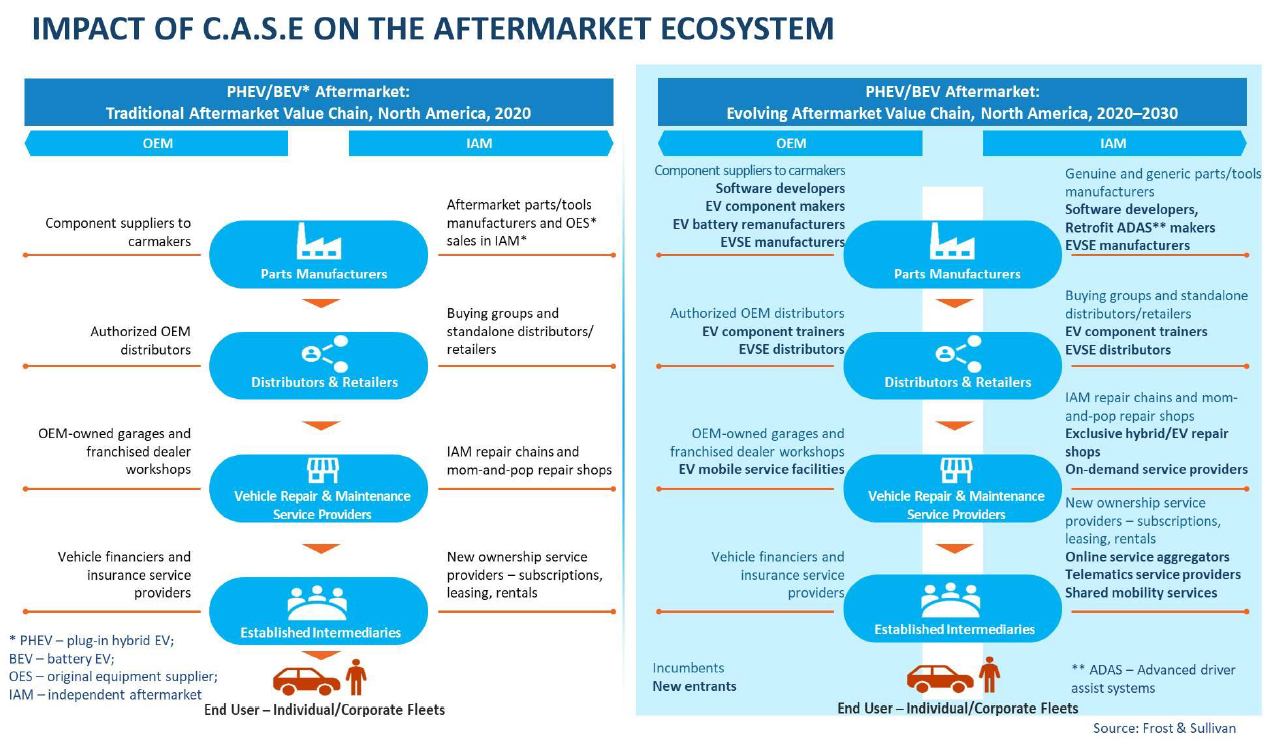

A new automotive ecosystem is emerging globally as a consequence of related, autonomous, shared and electric powered (Circumstance) mega developments, reworking the aftermarket in the approach. Conventional income streams created by inside combustion motor (ICE) motor vehicles are established to dry up nonetheless, electrification will unleash a flood of new advancement opportunities connected with servicing plug-in hybrids (PHEVs) and battery electric powered motor vehicles (BEVs). As new pockets of demand from customers arise, present corporations and the latest entrants in the aftermarket will be compelled to structure correct electrification-led organization styles.

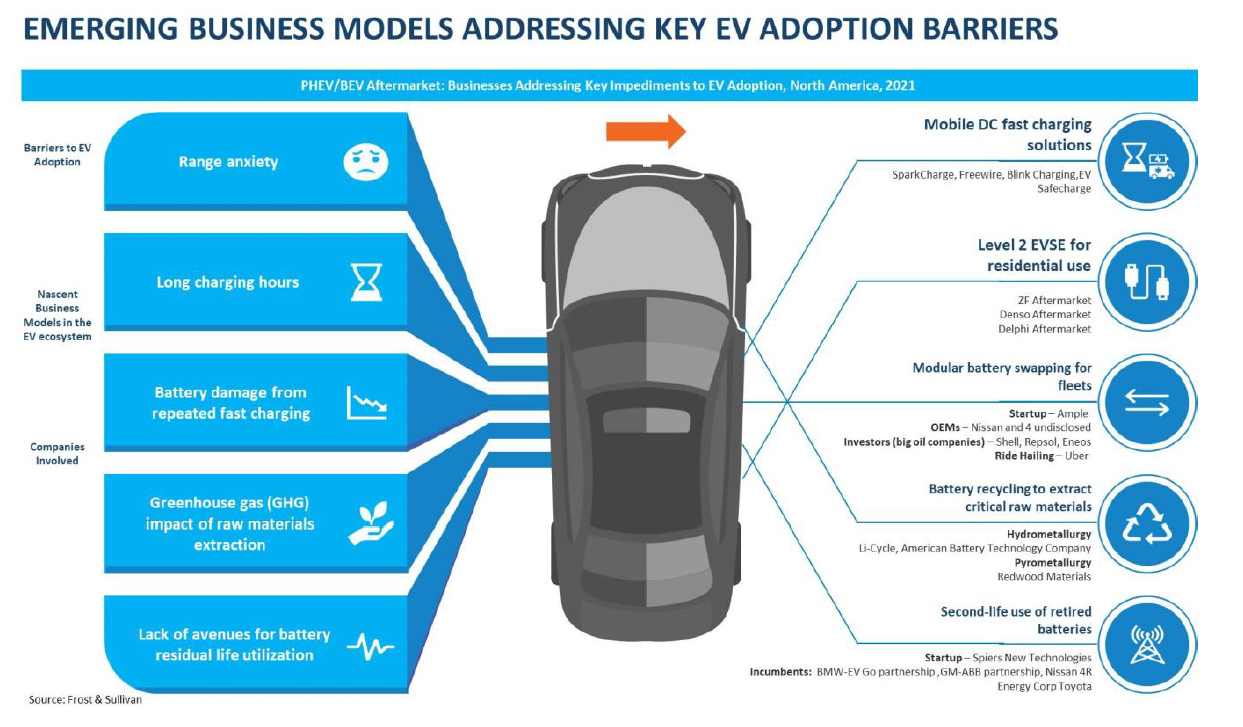

One of the most important restraints to the greater adoption of electric powered motor vehicles throughout most markets is the issue about battery selection. This has been generating the deal look like a trade-off involving a regular powertrain vehicle and an electric powered vehicle. It has, for that reason, develop into essential to tackle this challenge, primary to market place members discovering various organization styles.

Some of the most commonplace styles consist of furnishing economical cellular or at-home charging methods. This produces home for a assortment of members to enter the place and function with their very own worth propositions.

Some of the other organization styles about end-of-lifetime battery management have emerged as a necessity mainly because regulatory mandates compel market place members to be certain the harmless disposal of lifeless batteries.

Four key demand from customers pockets

Our most recent study identifies 4 vital parts of demand from customers: battery end-of-lifetime management, battery swapping for fleets, cellular DC charging, and Amount 2 Electric powered Motor vehicle Offer Machines (EVSE) retail that will supply healthy advancement potential.

Battery end-of-lifetime management that focuses on reusing and recycling, and modular battery swapping for trip-hailing fleets will demand huge upfront investments to scale functions.

Having said that, application-dependent, on-demand from customers DC rapidly charging (FC) and direct-to-customer product sales of Amount 2 EVSE that tackle selection anxiety will represent far more lower-hanging fruit, supplying far more quickly realisable ambitions for stakeholders.

Profits and advancement opportunities

In accordance to our estimation, the income chance dimension in North America alone could be USD2.one billion for Amount 2 EVSE retail, USD 972 million for battery end-of-lifetime management, USD 975 million for cellular DC charging and USD 347 million for battery swapping by the end of 2030.

In India, whilst the chance could be comparatively smaller, it will, nevertheless, represent an chance value tapping as problems bordering India’s large fuel import monthly bill, deteriorating air high-quality concentrations and spiraling fuel expenses gradually nudge personalized mobility preferences toward electric powered or hybrid possibilities. Sensing this, OEMs are diversifying their EV portfolios and the selection of styles available for the customers, catalysing EV adoption.

Based on developments, we expect battery end-of-lifetime management and cellular DC charging to be key aim parts for independent aftermarket (IAM) members.

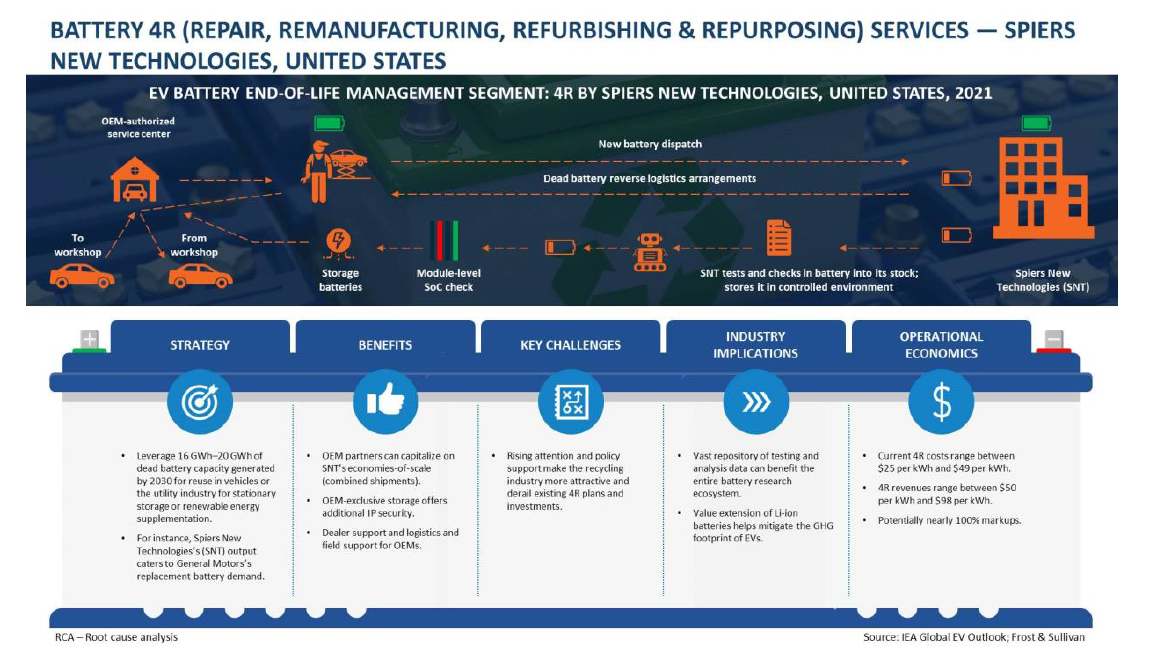

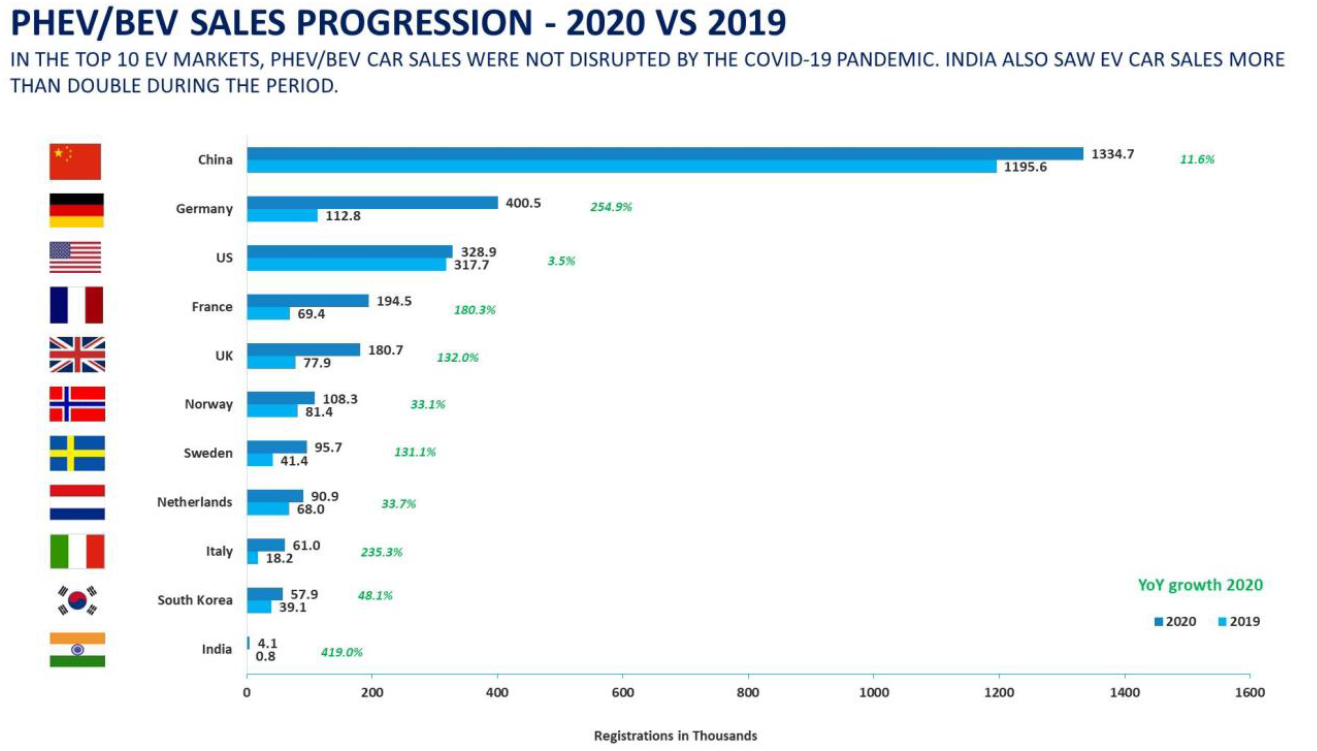

In 2020, roughly thirteen,302 EVs were being offered in India compared to 375,000 in North America. A cumulative retired lithium-ion battery potential of 19.four GWh is predicted in North America by 2030. We see members adopting 1 of the two methods for end-of-lifetime management of this potential. Each of them will demand distinct concentrations of scale and investments.

The initially will be battery recycling to extract critical uncooked elements from lifeless batteries and introduce them into new battery offer chains. The 2nd will be battery reuse as aspect of 2nd lifetime use in both equally automotive and non-automotive programs.

In India, the potential for deployment of retired EV battery potential for non-automotive applications gains even further significance when viewed versus the backdrop of the country’s renewable strength ambitions of setting up approximately 450 GW potential by 2030. This scale of deployment will generate a demand from customers for value-successful stationary storage methods, which the EV-retired batteries can give.

As aspect of its sustainability initiatives, Tata Substances is previously active in the lithium-ion battery recycling place, with its current aim predominantly on batteries extracted from customer electronics products. The corporation options to tap into retired EVs as a battery source for its functions the moment EVs go mainstream, creating adequate volumes.

Most of the current organization of Gravita India Ltd, the market place chief in India’s battery recycling place, will come from recycling direct-acid batteries. It is now eyeing the EV battery recycling chance and expects it to be a practical income stream by the end of the decade.

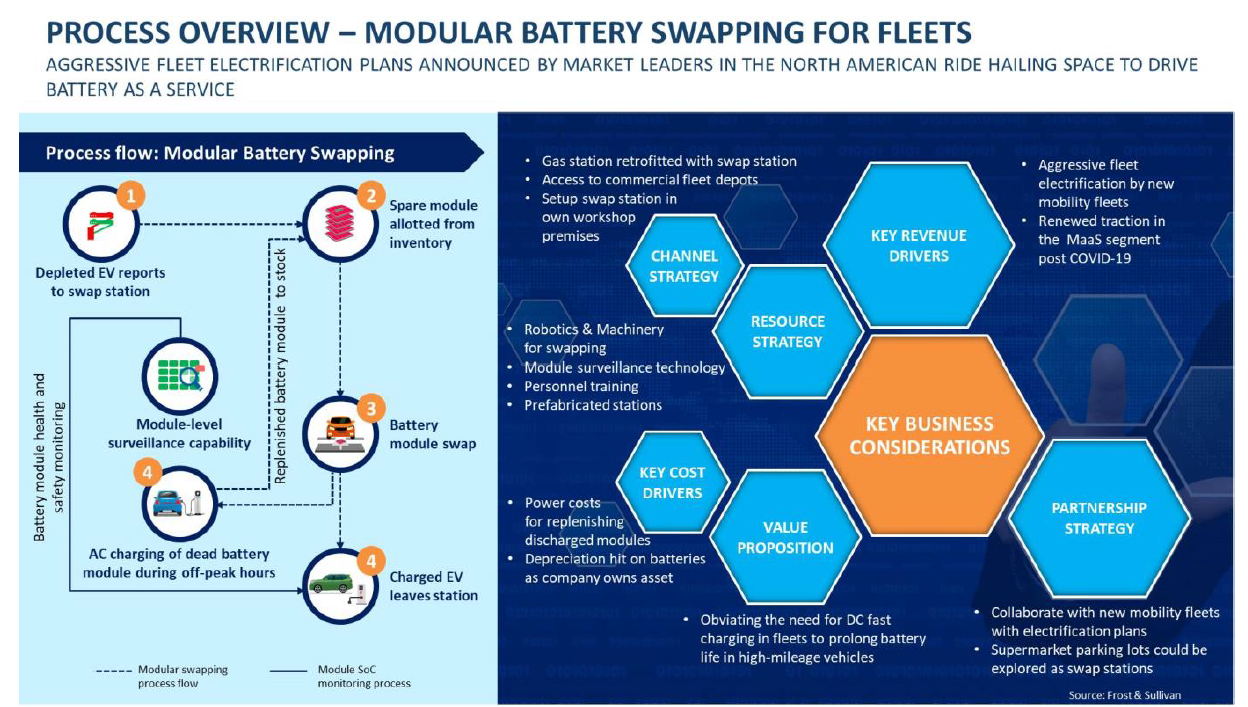

All symptoms level to the actuality that community direct current rapidly-charging (DCFC) infrastructure will be not able to preserve speed with the extraordinary advancement in PHEV/BEV vehicle parc. This will present sizeable and worthwhile organization opportunities for providers of B2C cellular DCFC—charging-as-a-provider, with off-peak charging keeping demand replenishment expenses lower.

Pretty much 70%-80% of the charging requires of PHEVs/BEVs are very likely to be addressed as a result of residential charging. As a result, we imagine that product sales of Amount 2 EVSE will supply a financially rewarding organization chance spurring residential customers to change to faster-charging machines such as Amount 2.

Battery swapping for fleet programs will be one more prospective advancement location. Shared mobility operators are major annual vehicle miles traveled (VMT) generators, averaging around 30,000 miles on a yearly basis. Major use, coupled with the adverse effects of recurring DCFC on battery lifetime, will underline the attraction of modular battery swapping as a practical rapidly-charging option for fleet requires.

A 2018 NITI Aayog review on shared mobility developments in India forecast an roughly 27% potential reduction in the cumulative vehicle kilometers traveled in a large-sharing scenario (a scenario in which there is large adoption of shared mobility methods like Uber and Ola), compared to the organization-as-typical scenario (a scenario in which the adoption concentrations will continue being as they are these days) by 2034.

In the meantime, trip-hailing players such as Ola and Uber are pursuing intense fleet electrification options as the environmental, social and company governance concept gains broader currency. For that reason, as city mobility turns increasingly toward shared and electric powered, battery swapping is predicted to come across favour among the drivers of shared EVs, supplying provider providers the reward of scale.

An additional location in which we are viewing OEM fascination is in totaled vehicle battery refurbishment, which entails the retrieval of usable EV batteries from full loss motor vehicles. This presents advancement opportunities and minimizes the worry on a battery waste management ecosystem that is only now gradually taking form.

5 advancement parts

Aftermarket members will also have to have to re-take a look at their procedures vis-a-vis the substitution of EV components. Indications are that the skills expected for producing EV components that combine with vehicle command devices will be the preserve of the OE channel, whilst the IAM channel will transform its awareness to remanufacturing for unsuccessful components that are not covered by warranties.

In line with this, Frost & Sullivan’s study highlights five key chance parts for aftermarket substitution. They are:-

- The failure of e-compressors in PHEVs/BEVs will generate opportunities for substitution with new/remanufactured components.

- The substitution of built-in starter generators (ISGs) in PHEVs.

- The substitution of electrical power electronics components like built-in inverters and DC-DC converters, whose extensive-phrase dependability is compromised by the warmth and have on-and-tear connected with large switching frequencies in EVs.

- Battery replacement—Repeated charging brings about a sizeable deterioration in the strength storage potential of EV batteries. A twenty five%-30% fall in authentic battery potential renders them unusable in automotive programs, ensuing in substitution with refurbished batteries with increased capacities.

- The substitution demand from customers for drive motors and reducers.

The bottom line

We will see an array of new demand from customers pockets and organization opportunities emerging for incumbents and new entrants in the aftermarket worth chain owing to the adoption of PHEVs and BEVs.

The options for the aftermarket to prosper and mature in a new period of electrified motor vehicles are serious and enormous. They consist of the customer readiness to transform standard ICEs to hybrid/EV variants as a result of do-it- by yourself (Diy) and do-it-for-me (DIFM) modes, cellular servicing for non-public EVs, dealership infrastructure updates to be certain preparedness for EV product sales, and servicing and smart methods concentrated on tyre lifetime optimisation technology for EV fleets.

What the aftermarket stakeholders have to have to do is to discover and leverage these embryonic opportunities with specific, electrification-led procedures.

(Disclaimer: Anuj Monga, Associate Director, Mobility Practice, Frost & Sullivan, has penned this report with contributions from Pranav Nair, Senior Study Analyst, Mobility Practice, Frost & Sullivan. Sights are personalized.)

Also Browse: